I initially warned about

U.S. bank bubbles bursting on

April 10, 2021. My follow-up to that was written on

October 15, 2022, which included detailed information on

BlackRock Inc.'s (

BLK) parabolic plunge.

Since then, we've seen another bank's demise unfold, namely, Silicon Valley Bank (SIVB)...the 16th largest bank in the U.S., and the largest bank by deposits in Silicon Valley.

It's interesting to note how closely SIVB mirrored the movements of Bitcoin, COIN, FNGU (10 Tech FAANG+ stocks ETF) and BLK, as shown on the following monthly comparison chart. They all rose and fell on parabolic movements...indicating a lack of investor confidence in their ability to retain any long-lasting sustainable value.

Their price action has, essentially, moved in lock-step with the S&P Regional Banking ETF (KRE).

Keep an eye on these in the coming weeks, inasmuch as a collapse in SIVB may trigger a contagion to other banks, including KRE, as well as FNGU, Bitcoin, and other crypto currencies and exchanges.

By the way, major support for KRE sits at 50.00, as shown on the following monthly chart. It's had difficulty holding onto, and adding to, gains made above that level since November of 2016.

A break and hold below could see price drop, in short order, to 40.00, or lower.

P.S. KRE gapped down and opened at 44.47 and hit a low of 41.98 in Monday morning trading...it's currently trading at 44.81 at 1:51 pm ET.

The following ZeroHedge articles provide background and current details on Silicon Valley Bank.

The following daily chart of USDC/USD depicts the de-coupling of the USDC 'Stablecoin' with the USD mentioned in the preceding article...one to watch, as well, for signs of continued or accelerating weakness.

P.S. More updates from ZeroHedge on Silicon Valley Bank...

P.S. Another bank bites the dust...Signature Bank (SBNY) has been closed...the 30th largest bank in the U.S., as of last year. The Wall Street Journal reported that, "Like Silicon Valley Bank, Signature relied heavily on deposits too big for FDIC insurance."

The price action in the following monthly chart of SBNY is pretty much identical to the others noted above.

It looks like

all of the DEPOSITORS at

SIVB and

SBNY will get

bailed out by the

U.S. Fed and

Treasury --

using taxpayers' funds -- as detailed in the following ZeroHedge article...

but, INVESTORS will NOT be part of that bailout. Yes,

it's really a bailout, and

American taxpayers will pay for it, according to

this ZeroHedge article.

By the way,

depositors with less than $250,000 at Silicon Valley Bank are already insured by the FDIC, so their money is

NOT at risk. However, reports indicate that

93% of depositors have OVER $250,000, so Biden is, essentially, bailing out his millionaire and billionaire Silicon Valley buddies, including California Governor Gavin Newsom and his three wine companies! Furthermore,

Chinese high-tech start-up companies also had money deposited at SVB, so, they will also be bailed out! And, so,

his government is

"full of fools to shield men from the effects of their folly," as they

"break down American capitalism," as more eloquently detailed in this

ZeroHedge report. And, on that topic,

Peter Schiff describes how the

"latest bank bailout is another nail in Capitalism's coffin" in this

ZeroHedge report. In fact, the news seems to be getting worse, as

another Biden scandal erupts, as described in this

ZeroHedge article.

I thought that after the last massive government bank bailout that occurred post-2008/09 financial crisis (for the banks deemed "too big to fail"), they assured American taxpayers that this would not happen again.

Somebody lied! If the

Fed STOPS raising interest rates because of this situation, you can be assured that

inflation will rocket upward...adding to

America's already-bloated national security risks.

Will heads roll at the Fed, including Chairman Powell, as ZH is calling for? After all, they (along with politicians' reckless fiscal policies and over-spending sprees, especially under President Biden these past two years) created the conditions leading to these banking failures, inflation, and chaotic mess!

ZeroHedge excerpt

ZeroHedge excerpt

ZeroHedge excerpt

Mount Printmore

* UPDATE March 13...

Trading in U.S. markets has been volatile and mixed...as traders/investors try to decipher all available information and consult their crystal ball to forecast various fallout scenarios from this hot mess and position themselves accordingly!

P.S. Another bank -- Silvergate Capital Corp. (SI) -- was originally co-founded as a savings and loan association in 1988. The company began providing services for cryptocurrency users in 2016, and conducted an IPO in 2019. In November 2022, concerns were raised about Silvergate's health, following the fall in cryptocurrency prices and the bankruptcy of FTX.

On March 8, 2023, the bank announced plans to wind down its operations and liquidate.

The following monthly chart of SI shows the spectacular parabolic spike and plunge of this bank.

This old saying is very appropriate to all things crypto, banks included..."If it's too good to be true, it probably is."

The following ZeroHedge articles provide further details in this regard.

So...that's at least three bank failures in the past week, alone.

The BIG QUESTION is: Are these bank failures a warning signal of systemic weakness in U.S. banks and the banking system, overall?

This ZeroHedge article provides one point of view on this question.

We'll see what happens in the coming weeks. No doubt, volatility will increase in all markets, for the foreseeable future.

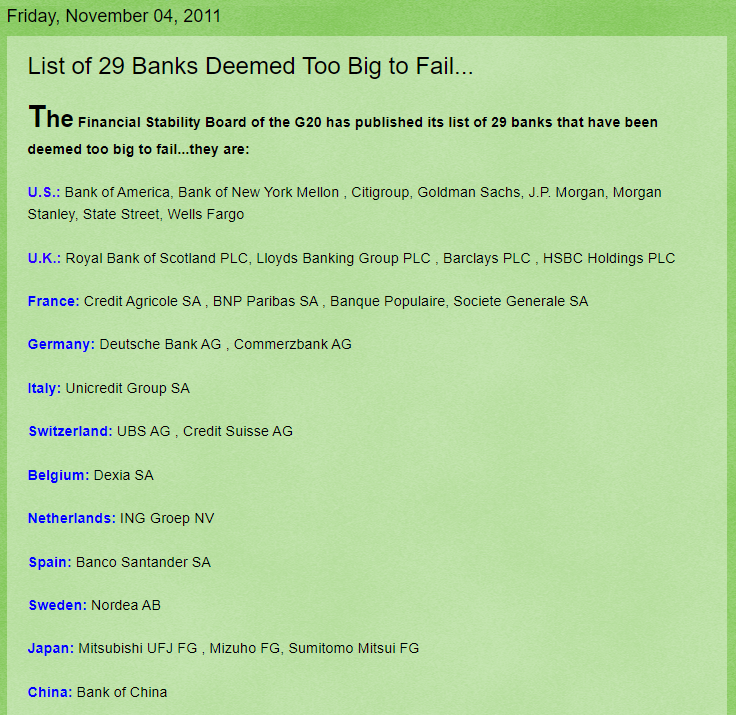

By the way, Silicon Valley Bank, Signature Bank, Silvergate Bank and First Republic Bank are NOT on the G20's list of 29 Banks Deemed Too Big To Fail. So, why are they getting "bailed out?"

* UPDATE March 14...

Economic data released this morning shows that inflation remains stubbornly high, while real earnings fell, as shown on the following economic calendar.

So, with banks now failing at the Fed's current interest rate of 4.5% to 4.75%, while annual CPI still remains high at 6.0%, (and Core CPI MoM actually rose higher in February) it seems that, on the surface, the Fed will be unable to raise rates any further without fuelling a contagion to other banks around the country. Although, we may still see further bank failures, regardless.

Exactly how the Fed expects to EVER gain control of high inflation is a mystery...especially with President Biden planning on spending $7 Trillion more in his next budget! 👀

By the way, with smaller regional banks failing, depositors are now fleeing with their money and putting it into the large too-big-to-fail banks, as described in this ZeroHedge report. So, is this really a subsidy of big banks, as alleged?

By the way, Congress and the Department of Justice need to investigate these bank collapses to determine whether anything nefarious was occurring that could have been prevented, had proper oversight been regularly conducted...then, report the truth to the American people.

American taxpayers (and investors) deserve that much, and more...instead of the gobbledegook currently being sold by the President and his minions (talking-head analysts and the mainstream press)!

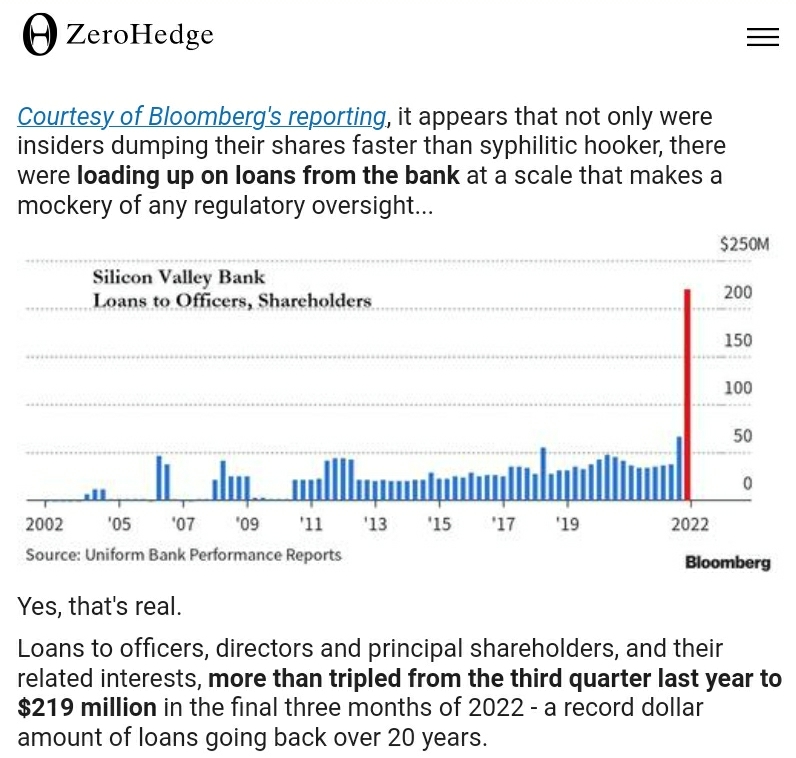

P.S. According to this ZeroHedge report, it seems that, "The DOJ and SEC are (separately) investigating the collapse of Silicon Valley Bank, focused on the possibility of misconduct by officers, including whether stock sales by executives violated trading rules."

N.B. This entire mess could have been avoided IF the Federal Reserve had stayed out of meddling with government bank bailouts and interest rates (holding them abnormally low or near Zero% from 2009 until six months after inflation hit with a vengeance in 2021, while engaged heavily in Quantitative Easing monetary policies)...and, instead, let the free market determine fair market value of equities, etc., to prevent overheating of markets and prices of goods and services, as well as tacitly enabling banks to take unmanageable risks on questionable or shaky loans and investments over the past 15 years.

Instead, it seems they've broken the financial markets, to try to stem and reverse Biden's runaway inflation caused by his excessive and unnecessary spending spree of Trillions of dollars over the past two years, as outlined in the following ZeroHedge article.

* UPDATE March 15...

Please see my post regarding Credit Suisse Bank at this link for important information regarding European banking weakness.

* UPDATE March 16...

Please see my post of March 16 regarding another Regional bank failure...namely, First Republic Bank.

* UPDATE March 21...

What on earth were Silicon Valley Bank executives, et al, up to in the weeks/months prior to its collapse?

Will any of their "unusual" activities ever be investigated?

Will anybody be held accountable for any banking violations, if they occurred?

If so, why were they bailed out?

ZeroHedge excerpt

Also, please see my post of March 21, which details the weakness in the KBW Bank Index.