My 2021 Market Wrap-Up and 2022 Forecast can be found at this link.

I speculated that 2022:

- would see higher volatility, lower volumes, lower trend sustainability, longer periods of consolidation, lower expectations, and lower certainty, overall,

- would be hung over with higher (persistent) inflation, COVID-19 variants and accompanying economic disruptions, increased interest rates, a changing political landscape, increasing national and international security concerns, and a skyrocketing national debt,

- may feel like market makers and movers/shakers have you "on hold" at times, and

- would bring surprises, some quite shocking (to markets) if/when they become common knowledge.

In conclusion, I suggested that traders/investors look for more stable and valuable sectors and stocks, commodities, bonds, and currencies which, potentially, may act as a safer hedge against the headwinds (and, as yet, unrevealed shocking surprises) described above.

In fact, 2022 ushered in all of these events.

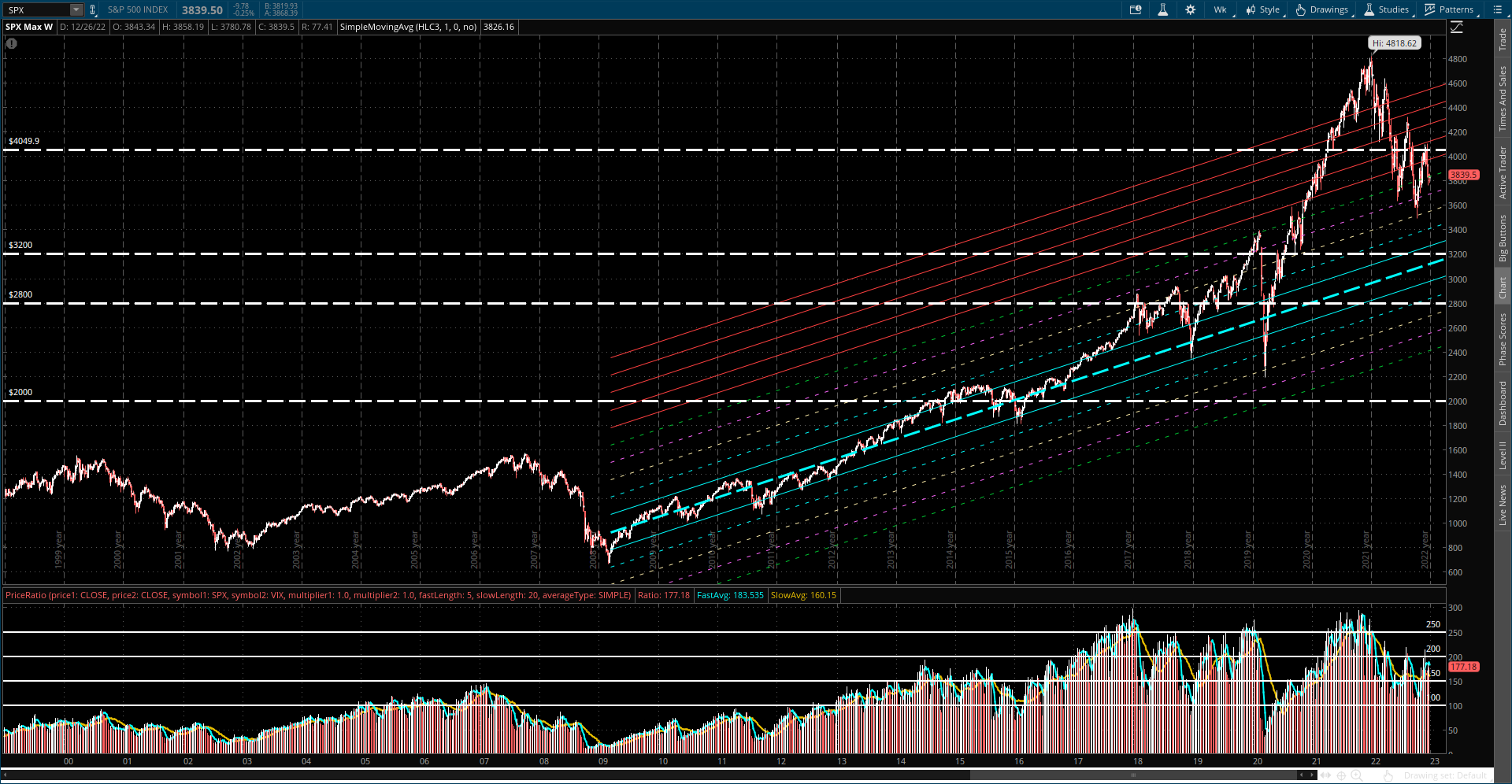

Large-scale whipsaw market action in 2022 is evident on the following weekly, monthly, quarterly and yearly charts of the S&P 500 Index (SPX).

My 2022 Market Wrap-Up post describes this more fully...2022 was a year of:

- a slow, choppy decline,

- day-to-day or week-to-week erratic and non-directional trading, with price bouncing back and forth between Buyers and Sellers, like a yo-yo, and

- gains on either the long or short side being short-lived.

Of the following graphs of the U.S. Major Indices and Major Sectors showing percentages gained/lost in 2022, the only sector that made any significant gains was the Energy sector (which gained 64.32%). All of the Major Indices lost, with the Nasdaq Composite and Nasdaq 100 Indices losing the most, while the Dow Utilities lost the least.

The U.S. Fed has continued to aggressively raise interest rates, which now sit at 4.25 to 4.50%. Its 2023 target rate is 5.1%...its 2024 target rate is 4.1%...and its 2025 target rate is 3.1%.

The COVID-19 virus has continued to play havoc with supply chains and world markets, especially, parabolic one-hit COVID-era wonders...as noted in these posts. China is struggling with a massive increase in the virus, which is causing great harm to its population, and has been having a negative effect on its Shanghai Index and Hang Seng Index.

President Joe Biden's economic agenda of out-of-control spending of trillions of dollars has shot up the U.S. National Debt to almost $31.5 Trillion, making every taxpayer responsible for $246,866+...and increasing the threat to National Security...as well as making life miserable for Fed Chairman Jerome Powell. Biden shows no signs of changing any of his extreme far-left (socialist) policies or agenda, which will lead to his eventual political downfall...he can kiss his 2024 chances of re-election good-bye!

Russia invaded Ukraine on February 24, 2022 in a major escalation of the Russo-Ukrainian War, which began in 2014...and has caused thousands of deaths on both sides, cost the U.S. and NATO countries billions of dollars, and has caused Europe's largest refugee crisis since World War II. As a result, Crude Oil prices shot up and will remain elevated, or climb higher, as long as President Biden and other world leaders continue their relentless war on fossil fuels in favour of pushing their climate-change theories and ESG agenda.

Record-high illegal border crossings, drug smuggling, and human trafficking operations along the southern border of the U.S. (approx. 5 million in the past 2 years from 161 countries), along with record-high violent crime rates and large-scale "looting swarms" of businesses all across America, are threatening to bankrupt many small businesses. If this continues unabated, along with rising interest rates, we'll see more and more layoffs this year in a variety of small and large companies (raising the unemployment rate), as well as higher prices of goods and services...leading to a recession and/or stagflation.

U.S. and foreign Banks are under pressure, as shown on the following monthly chartgrid, as interest rates rise and as businesses begin to default on loans and credit card debt repayments stop. Furthermore, if any of these banks are involved in crypto trading, as described below, we'll likely see further losses, if crypto contagion becomes widespread in 2023...etc.

The U.S. Dollar remains the favoured of world currencies, as shown on the following percentages gained/lost graph in 2022.

However, it has lost ground during the latter half of 2022, as other world currencies moved back toward their long-term "median" of their respective regression channels, as shown on the following monthly chartgrid.

2/5/10/30-Year U.S. Bonds peaked in 2020 and have dropped ever since, as shown on the following monthly chartgrid. However, they have stabilized somewhat just below their respective long-term regression channels. I think investors will start buying up Bonds in 2023, as crypto markets continue to fail, bank lending tightens, and equities continue to drop.

The crypto-currency markets were roiled by the Sam Bankman-Fried scandal involving FTX, et al, as described here. A related crypto-currency, Bitcoin, lost 64.07% in 2022, as shown on the Currencies graph above. No doubt, there will be more crypto contagion as more graft (corruption, deceit and fraud) is uncovered, along with reckless "investments"...and we may eventually see Bitcoin hit 10,000, or lower to, possibly, zero, as shown on the monthly chart below.

The following Pivot Points were calculated from the high/low/close of the 2022 candle, shown on the Yearly SPX chart above.

It shows the SPX target resistance and support levels for 2023. Note that S1 is close to the 3200 level, mentioned in my post of December 21. I think that level will be hit sometime in 2023...possibly the first half.

Rather, I think we'll see more of the same that transpired in 2022, as I described in my opening segment above, with choppy, whipsaw prices sliding down to 3200, or lower...particularly, as/if companies forecast lower earnings growth in their upcoming quarterly releases in 2023.

As in 2022, "look for more stable and valuable sectors and stocks, commodities, bonds, and currencies which, potentially, may act as a safer hedge against the headwinds (and, as yet, unrevealed shocking surprises...yes, more await), as described above."

Happy New Year and best of luck in 2023!

* UPDATE Jan. 16, 2023...

Well, that didn't take long...the first shocking surprise of 2023 has arisen...Joe Biden's Classified Document Dilemma. We'll see if there's any fallout in the markets, as a result, in due course.

* UPDATE Jan. 17...

From this Wall Street Journal article..."Big banks may need to be broken into smaller pieces if they become too big to manage and are unable to fix significant regulatory lapses, a top federal banking regulator said in a warning shot across Wall Street on Tuesday."

We'll see if this becomes another shocking surprise of 2023...see my above-mentioned comments regarding U.S. and foreign Banks on rising interest rates, loan and credit card defaults, crypto contagion, etc.

* UPDATE Feb. 5...

Please see my post of December 29, 2019 (SPX: What's In Store For The 2020s & 2030s?) for additional relevant information.

* UPDATE Feb. 7...

When consumers start defaulting on their credit debt (loans, car payments, mortgage payments, student loan payments, etc.), then the fireworks will begin and equity markets will tank.

P.S. Subprime auto loan defaults are beginning, as described in this Zerohedge article (Feb. 27).