* See UPDATE below...

In my post of March 14, I described a scenario where a drop and hold below 20,000 on China's Hang Seng Index (HK50) could see it plunge to 16,000, or lower.

It, subsequently, swirled around that level, finally closing below at the end of August, as shown on the following monthly chart.

It has since plummeted and closed on Monday at 15,180.69...losing 6.3% on the day.

Sellers are in control, as downside volatility is increasing.

Should price remain below 20,000, it could easily drop to 12,000, or even lower to 8,000.

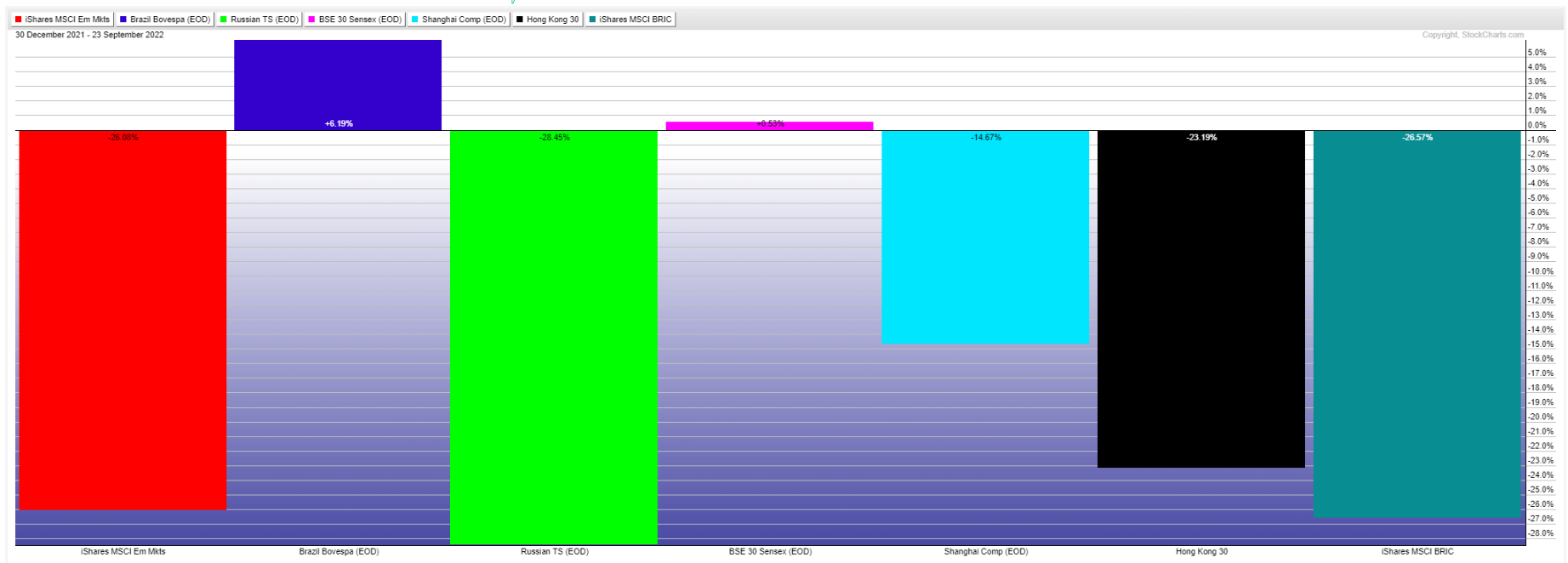

Monday was a bad day for all Chinese indices.

There are numerous major issues, with which China is grappling, including their property market, technology sector, zero COVID-19 policies, inflation, currency, support for Russia in their war with Ukraine, etc.,...none of which can be readily resolved...and none of which would be attractive to new foreign investment.

The following article describes some of those.

N.B. Further China weakness may drag other world markets (or their financial institutions) lower, if they are already heavily invested, directly or indirectly, in any of those markets.

So, bear in mind the remarks I made in my post of October 22.

* UPDATE Oct. 29...

The Hang Seng Index lost further ground this past week...opening below 16,000 and closing at 14,863.06.

It closed below the bottom of a long-term uptrending channel the prior week around the 16,500 level, as shown on the following monthly chart.

Any sustainable rally over the coming weeks will need to see it retake and hold above, firstly, 16,000, then 16,500...for a possible retest of 20,000.

Otherwise, it could easily plunge to 12,000, or, even, 8,000.

Correspondingly, the Shanghai Index (SSEC) is caught in a narrow band within a large matrix (between 3,000 and 2,840), as shown on the following monthly chart.

It's had difficulty remaining above 3,550 since January 2007, which is a formidable long-term resistance level (and part of a significant future apex within this matrix...forming roughly in April 2029).

Failure to convincingly retake and hold above 3,000, could see it plunge to 2,500, or, even, 2,000.

For now, China weakness continues.

* UPDATE Nov. 27...

From the following report, it's clear that the China boom of the 1990s, then the 2000s, has been badly damaged, as shown on the monthly chart of the Hang Seng Index (HK50) below.

HK50 has failed to continue with the upward trajectory and pace of those decades, evident by the break and plunge below the longterm rising channel this year.

Furthermore, HK50 has struggled to remain and gather strength above 20,000 for the past 16 years.

I find it hard to believe that China will regain its former glory any time soon, if ever, (a) for the reasons cited in the report, (b) for the aforementioned charting reasons, as well as, (c) the fact that world countries are moving away from their previous reliance on cheap Chinese goods in favour of domestic product development and production.

As such, I anticipate that HK50 will be locked in a large sideways trading range for some time -- complete with volatile whipsaw price action -- between 12,000 and 20,000.